Crypto Regulations in the United States 2025/2026: From Fragmentation to Market Structure

For more than a decade, the US crypto industry has existed in a strange legal limbo. Not illegal, but never fully legitimate. Not banned, but constantly under threat. Companies built, users traded, and capital flowed – all while regulators argued over who was actually in charge.

Unlike the EU, which chose a unified framework with MiCA, the United States took the opposite route. Regulation emerged piecemeal, agency by agency, enforcement action by enforcement action. The result is a system where the rules often depend on who is asking, which asset is involved, and which regulator decides to speak first.

That fragmentation is precisely what the new US crypto market structure bill is trying to fix.

Before we get to the bill itself, it’s worth understanding why the current system cannot work in future.

The Current US Crypto Regulatory Landscape

At the federal level, crypto in the US is regulated not by one authority, but by several. Each of them has its own mandate, interpretation, and incentives.

Key Crypto Regulatory Bodies in USA and Their Roles

| Regulator | Primary Mandate | Role in Crypto |

|---|---|---|

| SEC (Securities and Exchange Commission) | Investor protection, securities markets | Defines whether crypto assets qualify as securities and applies federal securities laws to protect investors, focusing on disclosure, registration, and enforcement where tokens resemble investment contracts [1]. |

| CFTC (Commodity Futures Trading Commission) | Commodities and derivatives markets | Oversees crypto as commodities, primarily through derivatives markets, while focusing heavily on fraud prevention and investor alerts in largely unregulated spot markets [2]. |

| FinCEN (Financial Crimes Enforcement Network) | AML / CFT compliance | Enforces AML and counter-terrorism rules in crypto, requiring businesses to monitor, report, and prevent illicit financial activity while balancing innovation with compliance [3]. |

| IRS (Internal Revenue Service) | Tax collection | Treats digital assets as taxable property, requiring individuals and businesses to report crypto income, wages, and transactions for federal tax purposes [4]. |

Each agency operates within its own legal mandate and scope of responsibility. None of them were originally designed for digital assets. And none of them have had clear congressional guidance on how crypto should fit into existing law.

The Result: Structural Confusion

- The SEC claims broad authority by applying decades-old securities law to modern blockchain assets.

- The CFTC oversees crypto derivatives but has limited authority over spot markets, mainly restricted to fraud and market manipulation cases.

- FinCEN focuses on compliance, not market structure.

- The IRS is about taxation, regardless of regulatory clarity.

For businesses, this means overlapping obligations and constant legal uncertainty. For users, it means protections depend on which platform they use and where the regulator draws the line that day.

This is the environment in which the US crypto market structure bill emerged.

USA Crypto Regulations: State-by-State Overview

In the United States, crypto regulation is not only fragmented at the federal level, but also varies significantly from state to state. While federal agencies like the SEC and CFTC set overarching rules, individual states often introduce their own legislation, licensing requirements, or consumer protections, creating a patchwork of regulations that businesses must navigate.

On the National Conference of State Legislatures (NCSL) website, you can track cryptocurrency-related legislation across all US states, including which bills have been introduced, advanced, or enacted, and their current status [5].

In 2025, at least 40 US states have introduced or are considering legislation related to cryptocurrency, digital or virtual currencies, and other digital assets. The pace and direction of regulation vary widely – from stricter oversight in some states to innovation-focused or exploratory approaches in others.

| State | Legislative Action / Focus | Notes |

|---|---|---|

| Arizona | Required crypto kiosk operators to disclose terms and use blockchain analytics | Also established Bitcoin & Digital Assets Reserve Fund |

| Arkansas | Amended Uniform Commercial Code | Clarified that “money” does not include central bank digital currency |

| Georgia | Created Senate Study Committee on AI & Digital Currency | Early-stage research & policy exploration |

| Iowa | Defined charges for digital asset kiosks | Provides clarity for kiosk operators and users |

| Michigan | Declared May 13, 2025 as Digital Asset Awareness Day | Symbolic promotion of crypto literacy |

| Nebraska | Adopted Controllable Electronic Record Fraud Prevention Act | Focus on fraud prevention in digital transactions |

| Oregon | Added article on controllable electronic records to Uniform Commercial Code | Expands legal framework for digital assets |

| South Dakota | Updated Unclaimed Property Act for virtual currency | Includes notice requirements for crypto holders |

| Utah | Authorized state treasurer to invest public funds in certain digital assets | Moves state funds into regulated crypto exposure |

| Wyoming | Prohibited state agencies from using public funds to test/adopt CBDCs | Limits government involvement in central bank digital currency |

The US Crypto Market Structure Bill: What the Latest Regulatory Update Means for the Industry

November 10 marked an important day for the cryptocurrency industry. This was when the Senate Agriculture Committee released the long-awaited US crypto market structure bill's discussion draft. Chair John Boozman and Senator Cory Booker spearheaded the release, responding to years of industry demands. This text landed – which builds on the heavy momentum of the House-passed CLARITY Act from July – immediately after the dust settled on the recent USA government shutdown resolution.

For the better part of a decade, the digital asset market has operated in a gray zone in the United States. Companies have found themselves caught in the crosshairs of conflicting agency guidance, never quite sure where the lines were drawn. This new bill attempts to draw them. It represents a critical move toward defining the jurisdiction of the Commodity Futures Trading Commission (CFTC) over the crypto spot market. If this bill makes it across the finish line, it could effectively end the era of regulation by enforcement on US cryptocurrency firms.

The primary goal is simple – Congress needs to delineate authority. Specifically, lawmakers are working to draw a line between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). Doing so is critical to eliminate the jurisdictional ambiguity that characterized the US crypto industry for years.

Cody Carbone, who leads the Digital Chamber, stressed the importance of this push. He described the text as the "most consequential roadmap" for institutions trying to integrate digital assets into their operations. He noted that it finally provides a step-by-step guide for compliance – something that has been absent for over a decade.

Recent regulatory developments are adding momentum to the crypto reform effort. In early December 2025, the US CFTC announced that spot crypto asset contracts will begin trading on CFTC‑registered exchanges for the first time, marking a major step toward regulated US markets and broader integration of digital assets into mainstream finance. This initiative complements ongoing consultations by the CFTC on using tokenized collateral, including stablecoins, in derivatives markets, reflecting a shift toward practical regulatory integration and financial infrastructure modernization.

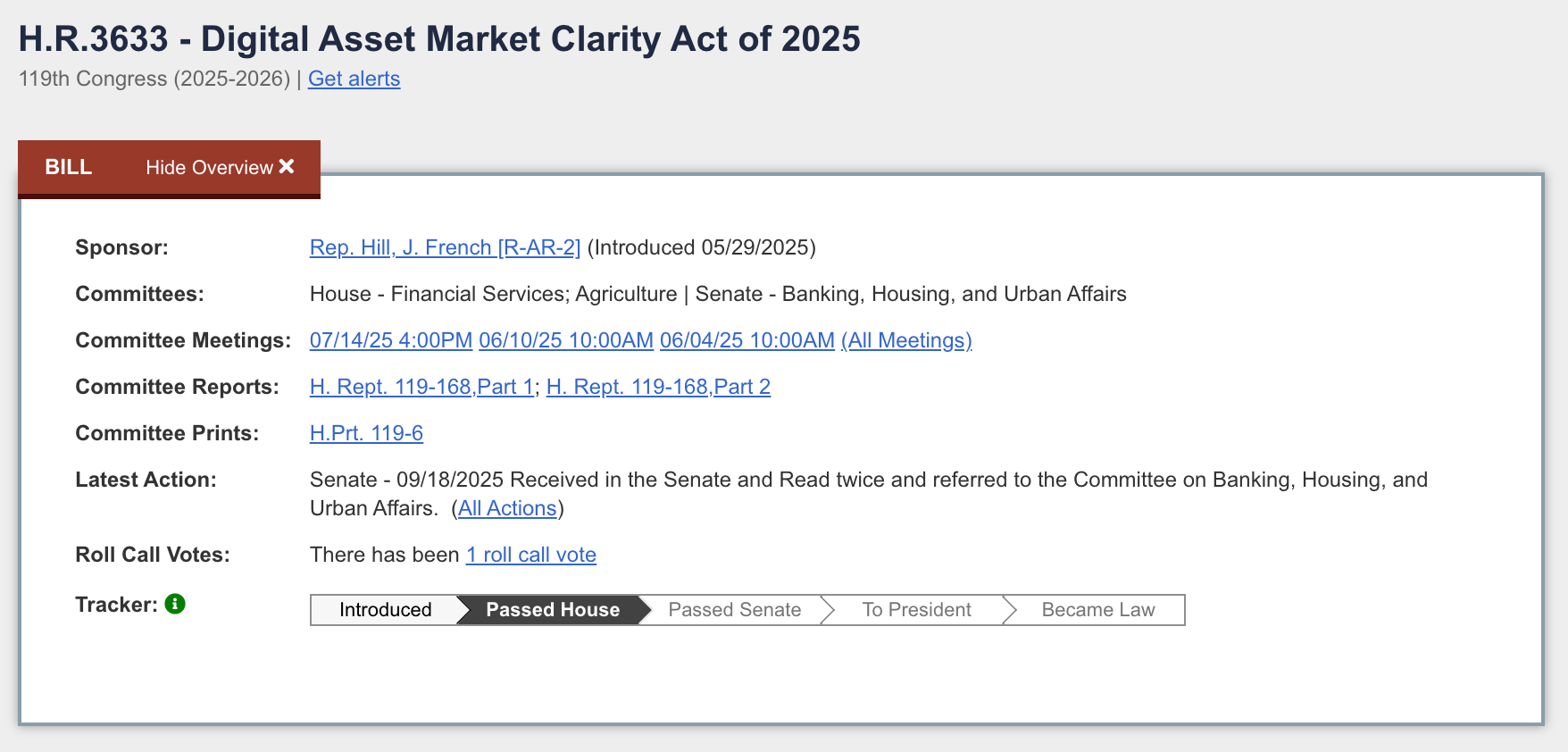

The path here has been anything but direct. A key precursor was the passage of the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins) in July. The House also moved its version of market structure laws forward. Also in July, the Digital Asset Market Clarity Act (CLARITY Act) passed with a decisive 294-134 vote:

The Senate Ag draft acts as a response to the House bill. It is built to be merged with legislation from the Tim Scott-led Senate Banking Committee, which oversees the SEC side.

The New Crypto Market Structure Draft

Released on November 10, the discussion draft of the crypto market structure bill is a joint effort from Senators Boozman and Booker. As part of a bipartisan approach, lawmakers are showing practical willingness to work across party lines to ensure regulatory clarity for the digital asset market.

The draft centers on granting the CFTC exclusive jurisdiction over digital commodities and spot market transactions. It defines a digital commodity as a fungible digital asset that can be owned and transferred between users without an intermediary and is recorded on a cryptographically secured public distributed ledger.

Key Regulatory Requirements

- Registration of digital commodity exchanges, brokers, and dealers

- Market surveillance obligations

- Fund segregation requirements

- Disclosure requirements for issuers and exchanges

- User fee funding model for the CFTC

Establishing a new registration regime is a major component of the draft. It mandates that digital commodity exchanges, brokers, and dealers register with the CFTC. Registration is not just a paperwork exercise; it means complying with core principles regarding recordkeeping, trade monitoring, and conflicts of interest. These entities will have to prove they can surveil their markets to prevent manipulation and fraud.

Consumer protections are front and center. The bill highlights provisions requiring the segregation of customer funds. This is a direct response to past industry incidents where platforms commingled user assets with corporate funds (such as in the infamous FTX scandal). The draft mandates strict disclosure requirements for token issuers and exchanges – ensuring that retail users have access to material information before they trade.

As the CFTC is a smaller agency than the SEC, funding this expanded oversight has always been a hurdle. The draft includes a provision allowing the CFTC to collect user fees from registered entities. This would fund the expanded oversight and address long-standing concerns about the agency's resource constraints.

Critically, the text contains bracketed sections. These are areas where the language is not yet finalized and is still under negotiation. You will find brackets specifically around the "security" definition and DeFi regulations. This is a clear sign that Congress is still debating where to draw the boundary between digital commodities and securities.

Amanda Tuminelli, who serves as Executive Director of the DeFi Education Fund, responded to the bracketed sections with cautious optimism. She stated they hope the section left open for DeFi will be filled with robust developer protections. She stressed the importance of distinguishing centralized intermediaries from software developers who do not hold custody of "other people's money."

Another bracketed requirement mentions that the CFTC must be fully constituted with at least two commissioners nominated. Currently, the agency remains understaffed despite recent leadership changes. Mike Selig has been confirmed by the U.S. Senate as CFTC Chair, replacing Acting Chair Caroline Pham, and will initially serve as the sole commissioner. This provision suggests that Congress wants a fully staffed agency before granting it massive new powers [16].

Impact on Exchanges, DeFi, and Custody

The heaviest burden will be on centralized exchanges (CEXs) under this new framework. CEXs must register with the CFTC, prove they don't commingle funds, and maintain substantial capital reserves.

This creates a regulatory moat around the US market. Only compliant, well-funded entities will be able to operate legally. While this increases safety, it also raises the barrier to entry for new competitors.

Juan Leon, an analyst at Bitwise, pointed out that these changes challenge the all-in-one business models that have dominated the crypto exchange market. He noted that requiring firms to separate distinct regulated functions would serve as a foundational pillar for institutional adoption.

That said, the situation regarding decentralized finance (DeFi) remains ambiguous and tense. A Senate Democrat proposal leaked in October 2025 suggested that front-end developers should be regulated as brokers, to which the crypto industry responded with outrage. Many argue that writing code is a form of free speech and that software developers should not be classified as financial intermediaries.

DeFi Regulatory Concerns

| Issue | Industry Concern |

|---|---|

| Front-end developers as brokers | Could chill innovation; free speech concerns |

| Ambiguous bracketed language | Creates uncertainty for DeFi builders |

| Risk of overregulation | Could push innovation offshore |

Summer Mersinger, CEO of the Blockchain Association, pushed back hard against the leaked proposal. She warned that it could effectively ban decentralized finance and wallet development in the United States. She argued that the language is impossible to comply with and would drive development overseas. The current Senate Ag draft leaves this section in brackets, suggesting the committee has yet to reach consensus on the provision.

This nuance is vital for DeFi projects. Keith Grossman, the President of MoonPay, stressed the need for legislation to separate centralized intermediaries from decentralized systems. He noted that this draft reflects a bipartisan understanding that applying a single set of rules to on-chain technology simply does not work.

Retail users could see safer markets under this legislation. Theoretically, there will be fewer rug pulls and better disclosures regarding the assets they buy. However, stricter listing standards could mean that some tokens get delisted from US exchanges if they don't meet the new bar. Retail traders might find their selection of assets on centralized platforms somewhat reduced compared to before the US crypto market structure bill.

This new regulatory environment highlights the critical distinction between custodial and non-custodial models. The bill's strictest rules target custodial intermediaries – entities like CEXs and other centralized finance (CeFi) providers that hold private keys on behalf of users. When a platform takes crypto in custody, they assume a fiduciary responsibility. This justifies the heavy compliance burden regarding fund segregation and capital reserves.

Non-custodial platforms face a different risk profile. Here, the user retains control of their private keys and digital assets at all times. Operating differently from the centralized platforms targeted by the bill, ChangeNOW serves as a prime example of a non-custodial exchange platform. As per the new draft, CEXs must overhaul their infrastructure to comply with segregation rules, but ChangeNOW's model facilitates swaps without holding user funds. This fits the ethos of self-custody that the legislation is trying to protect.

The draft also allows cryptocurrency trading across multiple infrastructure layers and blockchains – facilitated by services like ChangeNOW's multi-chain bridge. This allows users to move crypto seamlessly between different chains while avoiding the counterparty risks associated with centralized custody. As the rules for custodians get stricter, the value proposition of non-custodial and interoperable platforms becomes increasingly clear for users prioritizing self-custody.

Senate Pushes Crypto Market Structure Bill to 2026

The Senate has delayed any markup on the crypto market structure bill until early 2026, leaving a final framework for the industry just out of reach for now. Lawmakers continue negotiating key issues, including SEC and CFTC jurisdiction, market integrity, and financial stability, with bipartisan discussions described as “intense and ongoing.” [15]

Industry leaders see the delay not as a setback, but as a sign that careful, bipartisan policymaking is underway, setting the stage for a durable, consumer-friendly, and innovation-focused framework in early 2026.

Risks, Opportunities, and the Path to 2026

The opportunities presented by this bill are significant – and institutional entry is perhaps the biggest potential upside. Analysts from Bitwise have suggested that clearly defining digital commodities will allow traditional financial institutions to confidently enter the market. Juan Leon from Bitwise explained that once this bill passes, compliance and risk departments will finally have a federal statute to reference. He predicts this will shift internal conversations at major banks.

Clarity is another major benefit:

- It removes the shadow of regulation by enforcement that has hung over the industry.

- Under the previous leadership of the SEC, US businesses have been hesitant to build or launch products for fear of sudden lawsuits from regulators.

- A statutory framework allows crypto market players to innovate with a clearer understanding of the rules of the road.

Risks to Consider

Despite the opportunities, there are real risks that could impact the market:

Potential DeFi Ban

- A major risk is the "front-end as broker" definition, which could force developers to register as brokers simply for creating user interfaces.

- This would drive DeFi innovation offshore and could harm the US in the next wave of financial technology.

Compliance Costs

- High fees and registration costs could hurt smaller startups.

- If the cost of compliance is too high, it could lead to market consolidation, where only large incumbents can survive, reducing competition and innovation.

Political Conflicts

- There is significant friction regarding President Trump's connection to World Liberty Financial. Senators like Elizabeth Warren and Jack Reed have raised concerns about potential conflicts of interest.

- They questioned whether the venture’s token sales could facilitate sanctions evasion and emphasized the need to prevent crypto interests from profiting at the expense of US national security.

These political clashes may stall bipartisan cooperation, which is crucial for passing the bill.

CFTC Leadership and Staffing

The success of the bill depends heavily on leadership at the CFTC:

- The CFTC's expanded mandate requires a fully staffed agency to manage the new regulations effectively.

- Mike Selig, nominated as CFTC Chair, is awaiting confirmation.

- Additionally, the agency needs sufficient staffing to execute the regulatory framework.

The bill's effectiveness will rely on the CFTC’s readiness to handle the new responsibilities.

Conclusion

In summary, while there are significant opportunities tied to this bill – particularly with respect to institutional adoption and clarity in regulation – there are also real risks, particularly for DeFi and smaller startups.

The final outcome will depend on how well Congress navigates these risks and the complex political environment. If passed, the bill will set the stage for a new era of regulated digital asset markets, balancing safety with innovation.

Resources

- SEC Crypto Task Force

- CFTC Digital Assets

- FinCEN Readout: Public-Private Partnership to Promote Innovation

- IRS: Reporting Crypto and Other Digital Asset Transactions

- NCSL: Cryptocurrency, Digital or Virtual Currency, and Digital Assets 2025 Legislation

- Senate Agriculture Committee: Boozman & Booker Release Bipartisan Market Structure Discussion Draft

- US House Passes Crypto Market Structure Legislation, Moves on to Stablecoin Vote

- Congress.gov: House Bill 3633 (119th Congress)

- Reuters: US House Vote on Government Shutdown Deal

- CNBC: Five Takeaways from the Release of a Much-Awaited Crypto Market Structure Bill

- White House: Fact Sheet – GENIUS Act Signed into Law

- CNBC: FTX Bankruptcy Filing

- CoinDesk: Senate Ag Releases Long-Awaited Version of Crypto Market Structure Legislation

- CoinDesk: Senate Democrats Leaked Crypto Position Would Strangle DeFi Industry

- Senate punts crypto market structure bill to next year

- Binance post